What is Costs

Revenue, Cost and Profit

Economists often assume that the goal of enterprises is to maximize profits, and this assumption can work well. But what is profit? Here are some definition.

- Total revenue: The amount of money an enterprise obtains from selling its products.

- Total cost: The amount of money an enterprise spends to purchase inputs.

- Profit: Total revenue - Total cost

Generally, the total revenue is easy to calculate, It is equal to the output multiplied by the price of products, but the total cost is not so easy to calculate.

Opportunity cost

The opportunity cost of thing is everything else that must be given up in order to get it. This cost can be divided into explicit cost and implicit cost.

- Explicit cost: The input cost of the enterprise’s expenditure currency.

- Implicit cost: The input cost that do not require corporate expenditure currency.

Interestingly, the difference between explicit cost and implicit cost emphasizes the important difference between economists and accountants in analyzing business activities. Economists pay attention to studying how enterprises make production and pricing decisions. This decision will consider both explicit cost and implicit cost. In contrast, accountants’ work is to record the monetary factors flowing into and out of enterprises. They measure the explicit cost and often ignore the implicit cost.

Economic profit and accounting profit

- economic profit: Total revenue - Explicit cost - Implicit cost

- accounting profit: Total revenue - Explicit cost

In contrast, economic profit is more important in enterprise management. Enterprises that obtain positive economic profit can make up for all opportunity costs and leave some income as the reward of enterprise owners. When an enterprise has economic losses, even if it has positive accounting profits, it often has to withdraw from the industry.

Production and cost

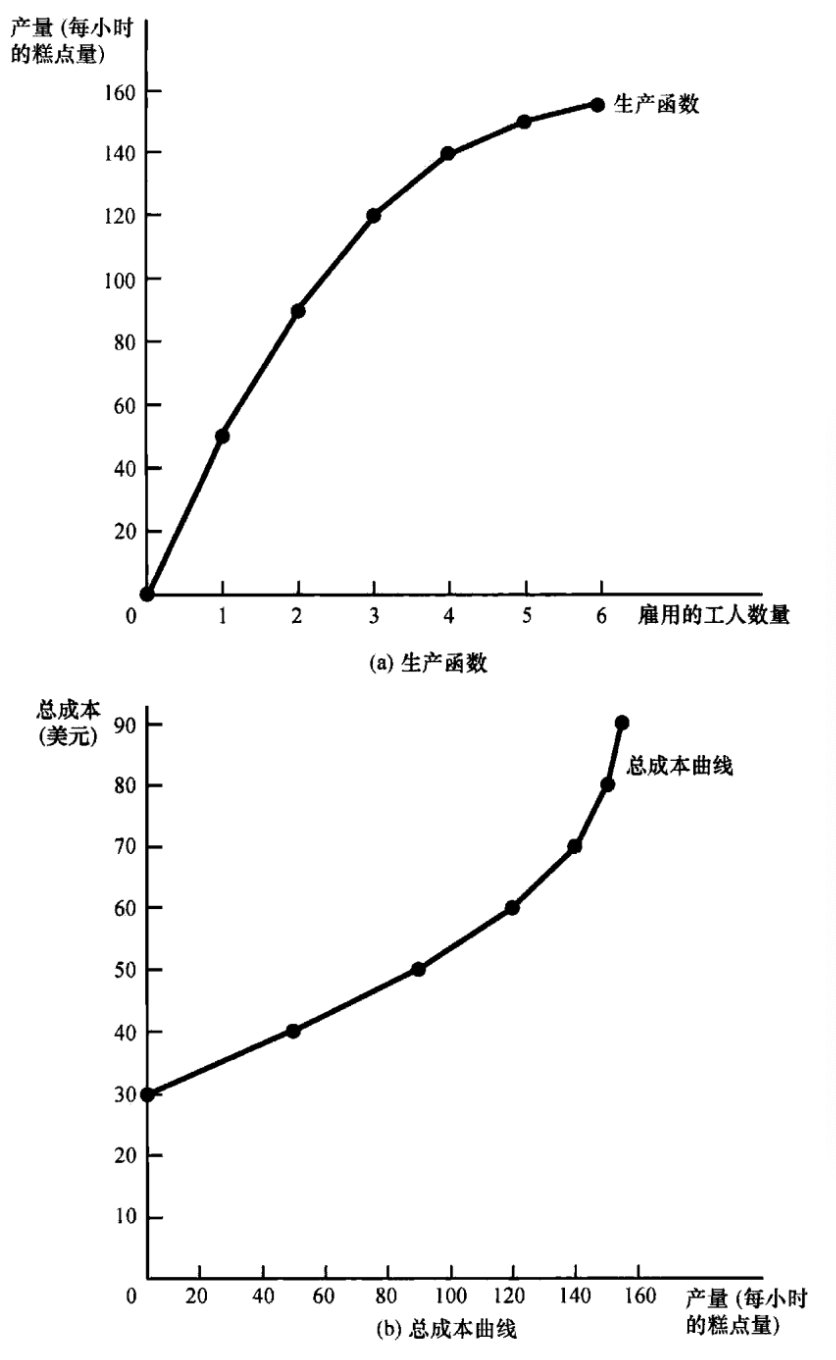

Produce function

In order to measure the relationship between the input and output of a production, the concept of production function appears. The marginal output of any input in the production process is the output increased by unit input, that is, the slope defined mathematically.

It is worth noting that with the increase of the number of workers, the marginal output of workers decreases gradually, which is called diminishing marginal output.

Total cost curve

Because the cost has a certain scale effect, the marginal cost will be smaller and smaller whit the increase of output.

If the production function and total cost function are placed in the coordinate system. With the increase of output, the total cost curve will become steeper and steeper, and the production function will become smoother and smoother. As shown in the figure below.

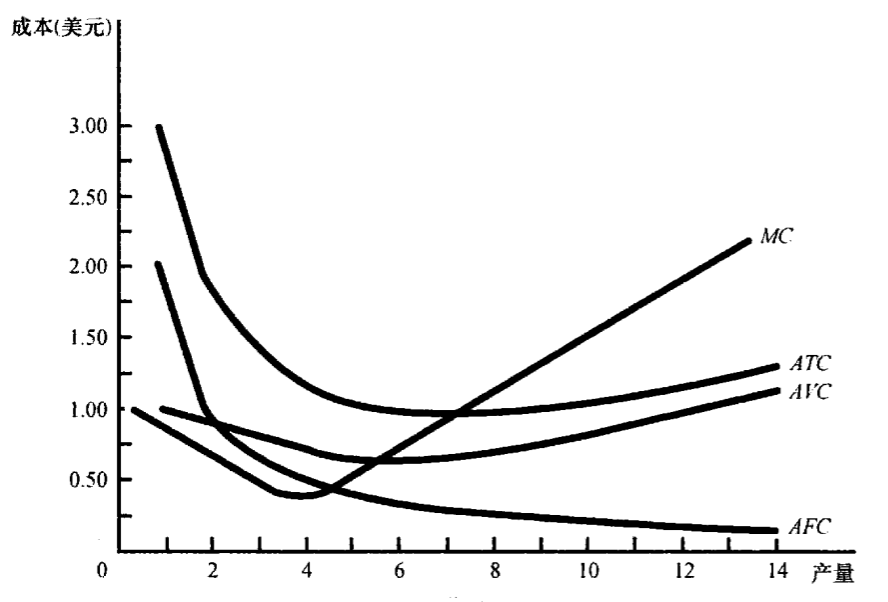

Various measures of cost

Fixed costs and variable costs

- fixed costs: cost that dose not change with the change of output.

- variable costs: cost that vary with production.

Average cost and marginal cost

- Average total cos (ATC)t: total cost divided by production.

- Average fixed cost (AFC): fixed cost divided by production.

- Average variable cost (AVC): variable cost divided by production.

- marginal cost (MC): total increased cost of one additional unit.

Cost curve shape

The cost curve of a typical enterprise is shown in the figure below.

It should be noted that:

- As production increases, the marginal cost will eventually rise

- The average total cost curve is U-shaped

- The marginal cost curve and the average total cost curve intersect at the lowest point of the average total cost curve.

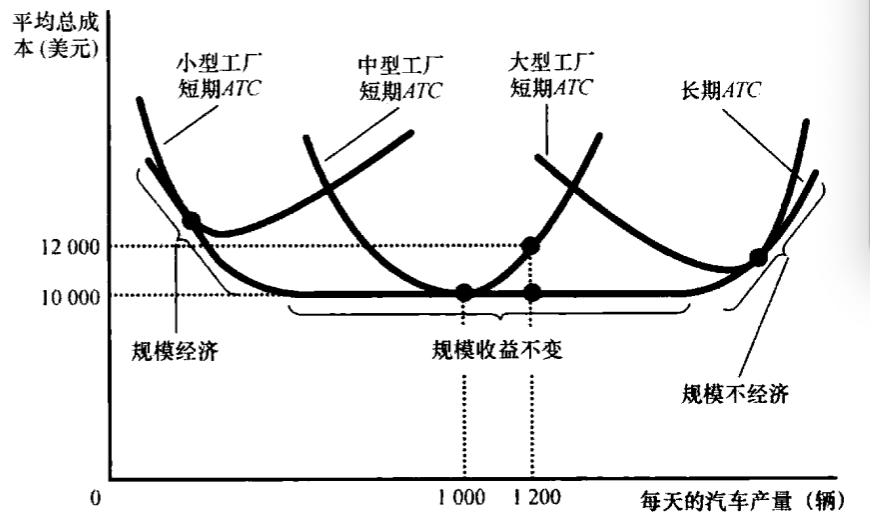

Short term costs and long-term costs

Relationship between different time length and average total cost

For many enterprises, the division of total cost between fixed cost and variable cost depends on the time range. Taking an automobile manufacturer as an example, the way to produce more cars in the short term is to hire more workers in the existing factories. Therefore, the cost of the factory is a fixed cost, but in the long run, the company will expand the scale of the factory, and the cost of the factory is a variable cost in the long run.

Economies of scale and diseconomies of scale

- economies of scale: The long-term average total cost decreases with the increase of production

- diseconomies of scale: The long-term average total cost increases with the increase of production

- constant returns to scale: The long-term average total cost remains constant when output changes

end~